FINA Committee Report

If you have any questions or comments regarding the accessibility of this publication, please contact us at accessible@parl.gc.ca.

Let me assure you we will give a full accounting to Canadians. They deserve nothing less. Finance Minister Paul Martin

Every effort must be made to avoid a deficit in this fiscal year and the next one.

Vancouver Board of Trade

In the aftermath of the tragedy of September 11 and in the midst of an economic slowdown, it seems difficult to believe that a year ago the economic picture was almost uniformly rosy and security issues were far from almost everyone’s mind. The economy was enjoying its 22nd quarter of uninterrupted growth, inflation was tame, the Department of Finance was predicting a cumulative surplus of $43 billion through to 2004-05 even after the tax cuts and spending increases announced last fall,[1] and the unemployment rate had fallen to 6.8%, its lowest level since 1974. If anything, the main policy concern seemed to be how to keep the economy from overheating. As David Dodge noted recently, “Around this time last year, both the Canadian and U.S. economies were pushing against or through their capacity limits.”[2]

These strong fundamentals demanded a policy shift from the spending cutbacks and tax increases of the mid-1990s to an emphasis on productivity and innovation, which in turn rested on tax cuts coupled with increased strategic spending on research, development, innovation and health care. This Committee was quick to seize on this new reality. In its 1999 pre-budgetary report New Era…New Plan, we wrote that the positive economic fundamentals of the previous three years were “no mere short-term anomalies” and that the goal going forward must be to “consolidate past achievements, further strengthen our economic performance, increase prospects for the future and hence help to secure what many Canadians view as the essential character of our economy and society.”[3] The Committee also cautioned, however, that history shows “nothing should be taken for granted” and that considerable long-term challenges remained in terms of Canada’s productivity performance and its competitive position.

The Rationale for a December Budget

We’re very pleased that the minister announced that the government intends to table a budget before the end of the year. Nancy Hughes Anthony, President and Chief Executive Officer, Canadian Chamber of Commerce

One of the things business hates the most is uncertainty. Certainly I think one of the kudos I would give to our central bank is that, if anything, they are consistent and very certain. Michael Atkinson, President, Canadian Construction Association

The September 11 terrorist attacks ushered in a new economic context and therefore a new set of priorities, showing just how appropriate earlier notes of caution were. The attacks and their aftermath demand a response to quell the uncertainty that makes long-range business planning difficult.

They have also made an already weakening economic situation worse, temporarily shutting down production facilities, threatening the viability of airlines at home and abroad, requiring new military and security expenditures, and slowing shipments of goods across the border.

The budget is the main economic event in Canada. It is the tool by which the government signals to Canadians its plans and priorities. This in turns helps consumers and businesses plan for the coming year. Even before September 11, Canadians were becoming concerned about the state of the economy, and the terrorist attacks on the U.S. only exacerbated these concerns.

In light of the current uncertainty all Canadians are facing, the Committee welcomes the Finance Minister’s October 24 announcement that he will present a budget in December. Echoing the voices of other Canadians, we believe that a December budget is instrumental to maintaining confidence in the economy.

The events of September 11 and its aftermath cannot be allowed to cloud or obscure this committee’s long-standing, long-term policy objectives, nor should it weaken our resolve to maintain and bring about the conditions required to make those goals a reality. This Committee believes that increased security and military expenditures in the short term are necessary to reduce uncertainty and to create the conditions for the broader, longer term objectives of strong productivity growth and higher standards of living. National security is a public good. It constitutes a form of social capital that is an important input into the national economy. While this has always been the case, it is increasingly so today as real and perceived terrorist threats are having a significant impact on the day-to-day operation of the economy as well as business and Consumer Confidence.

Assuring this future also means maintaining our commitment to the $100 billion tax reduction plan and $23.4 billion in increased health care spending announced last year, all the while maintaining our fiscal integrity and discipline by avoiding a deficit — the same fiscal discipline that helped Canada weather the 1997-98 Asian financial crisis and which will help us weather this crisis as well. That is the challenge facing Canadians and their government and which this Committee, in this pre-budgetary report, will tackle.

There are those who say that to counter the slowdown now we should cut taxes more or that we should spend more. In other words, that we should take the chance of going back into deficit. Well, that we will not do. We will not put at risk all that Canadians have worked so hard to achieve over the past few years. Rather, we will maintain the approach that has seen us through the peso crisis of 1994 and the Asian crisis of 1997, and which will see us through the current slowdown. Finance Minister Paul Martin, Economic Update

We’re now in the position where we can let the automatic stabilizers work … . I think that what is critical is that the government makes those expenditures that will help us with long-term problems. David Dodge, Governor, Bank of Canada

…it is clear that providing security will add greatly to the government’s expenditures, while the drag on economic activity caused by the attacks will reduce the revenues that Ottawa might otherwise have anticipated.

Canadian Manufacturers and Exporters

I think you should be cautioned against postponing future tax cuts simply because you see the economy weakening … . I think you should at least stay the course with your five-year tax reduction plan. Indeed, economic weakness is a justification for bringing forward future tax cuts that might be planned anyway. Thomas Wilson, Director, Policy and Economics Analysis Program, University of Toronto

Setting priorities for this budget cycle is a Herculean task indeed, but the immediate challenges should not inhibit the government’s ability to set out longer-term priorities for the economy. Elyse Allan, President and Chief Executive Officer, Toronto Board of Trade

Now is not the time to contemplate new multi-year spending. We believe that to do so would put tax cuts and Debt reductions at risk. Pierre Brunet, Vice-Chair, Board of Directors, Canadian Institute of Chartered Accountants

The Art of Forecasting

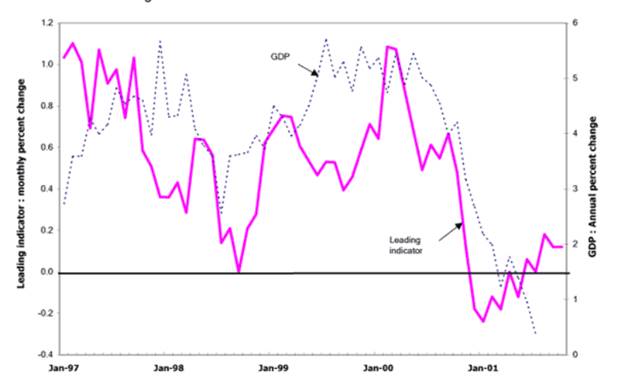

The rate of economic growth (measured as monthly changes from the year previous) started to decline in the middle of last year to levels that are generally considered more sustainable. The fall in growth rates continued throughout this year, to levels below capacity growth, and was presaged to some extent by the index of leading indicators, a barometer of where the economy may be headed.

The Leading Indicator Explained

By some accounts, economists and statisticians have been constructing leading indicators since at least the 1920s. This is not altogether surprising given the cyclical nature of market economies fl people have always wanted to know whether the economy was on the cusp of recession or a period of sustained growth. Leading indicators are generally built to answer that question and predict the general direction of economic growth over the course of the next three to six months. In other words, they are best viewed as predicting “turning points” between growth and recession or vice-versa rather than the “absolute value” of GDP six months down the road.

There are many kinds of leading indicators, although most versions represent “composites” or amalgamations of various data series that are most sensitive to the economic cycle. Statistics Canada’s leading indicator is a composite of ten such series, including furniture and appliances sales, sales of “other” consumer durables, money supply growth, changes in the Toronto Stock Exchange 300 Index, new orders for consumer durables, shipments-to-inventories ratio, the work week in hours, personal services employment, house spending, and an index of the U.S. economy.

Chart 1, which juxtaposes year-over-year changes in Gross Domestic Product (GDP) with monthly changes in the leading indicator, shows that the leading indicator turned down sharply in the late summer of 2000. The leading indicator, while negative for most of 2001, has most recently levelled off and showed some signs of improvement, suggesting the economy could begin to recover sometime next spring, as most forecasters now seem to expect. A note of caution however: the data for September do not reflect the full effects of the September 11 attack, suggesting the indicator could reverse some of its recent gains when the next round of data are released in late November. At the time of writing, real GDP growth in August from July was a faint 0.1%.

The leading indicator, however, is only a barometer of the economy’s direction or the general trend. It does not lend itself to easy quantification, an essential component of the budget-making process. The Department of Finance instead relies on a number of economic forecasts by private-sector economists. However, forecasting is fraught with problems and is an imprecise art at the best of times. At any given moment there is conflicting evidence as to the overall direction of the economy, with some forecasters choosing to highlight the negatives and some the positives. In an environment of heightened uncertainty, forecasting becomes even more difficult.

Chart 1: The Leading Indicator

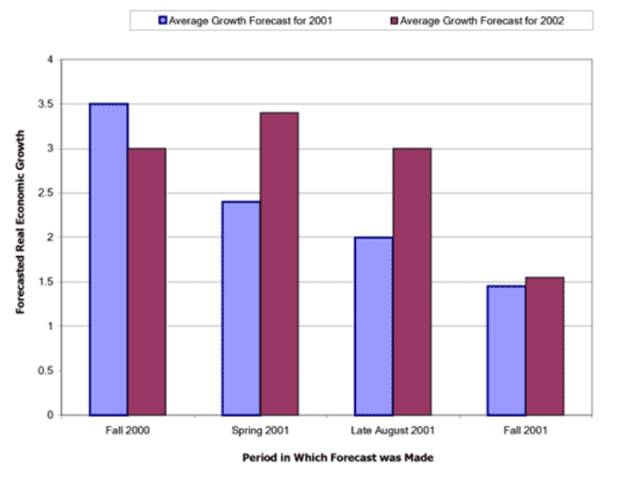

Last fall, the average forecast for economic growth for 2001 was 3.5%, notwithstanding the abrupt drop in the leading indicator. By May 2001, however, the average forecast was revised down to 2.4% after a spate of bad economic news. By late August, the average forecast had fallen to around 2%, again on the heels of more bad news.

With the events of September 11, the art of economic forecasting more than ever approximates something closer to guesswork than informed analysis, and forecasters have again revised down their forecasts, with the average now at less than 1.5%, or more than 35 basis points (i.e., 0.35 percentage points) below the “lower growth scenario” of 1.8% used by the Department of Finance in its May Economic Update and well below estimates of Canada’s potential growth rate of 3% a year.[4] Chart 2 shows the evolution of private-sector forecasts since September 2000. It is interesting to note that initially, forecasts became more pessimistic for 2001 but remained optimistic for 2002, indicating a quick rebound in economic activity. Recent forecasts are qualitatively different as they suggest lower growth for both years.

Chart 2: The Evolution of Growth Forecasts for 2001 and 2002

Despite the short-term gloom, most forecasters remain optimistic that economic growth will be robust by the second half of 2002 as tax cuts, lower interest rates and increased government and consumer spending take hold. Since the beginning of the year, short-term interest rates have been reduced by 450 basis points in the United States and by 300 basis points in Canada. The effects of monetary actions are well known to operate with a lag that can vary from instance to instance. The effects of these cuts should be evident in late 2002 and 2003, when growth is expected to reach 3.3%, slightly above the Bank of Canada’s calculation of non-inflationary capacity. In 2002, the average forecast has fallen dramatically to 1.64% from 3.4% in May.[5]

A recently released fiscal outlook published by TD Economics[6] provides a cautionary note in predicting that the state of the economy will drive the government sector (i.e., the combined federal and provincial budgets) into a planning deficit — i.e., a deficit before contingency and economic prudence — by 2002-03. Similarly, Patrick Grady, an Ottawa-based economic consultant and former senior official at the Department of Finance, forecasts that even before the recently announced security and airline measures, the government will post a surplus of $3.2 billion, which translates into a planning deficit of $0.8 billion for 2002-03.[7] These projected planning deficits demonstrate the fragility of the fiscal position of the government sector in Canada and its ability to forge ahead with aggressive Debt reduction.

Whether or not the federal government runs deficits in the future will depend upon its assessment of short-term security needs and the amounts to be spent and its ability to find savings elsewhere in the event that security needs grow substantially. New spending measures extending to fiscal year 2003-04, however, will threaten continued Debt reduction.

The TD Economics status quo projections see all government program spending increasing by 4% per year until 2005-06. For the federal government, this represents a $28 billion increase in program spending from 2000-01 figures, based on existing, non-security related commitments.

Finally, it is also worth noting that since 1992, the Canadian economy has grown at an annual rate of 3.3%. Forecasters therefore seem to be expecting Canada to resume “trend growth” by 2003 and that the current slowdown is only a temporary and possibly relatively benign — from a longer-term economic perspective — setback.

While it is impossible at this time to know with any precision the extent of the loss to the Canadian economy as a result of the events of September 11, it is clear that the figure is in the billions of dollars. The recession that was already evident in Canada’s manufacturing and exporting sectors during the past summer will be deeper and more prolonged than originally expected.

Canadian Manufacturers and Exporters

However, it must be stressed that these medium and longer-range forecasts, especially during times of great uncertainty, should be viewed with caution. For example, Merrill Lynch Canada told its clients in late September to “beware of the mantra that the recession will necessarily be “mild and mellow” or “short and shallow,”a view that has persisted in some quarters despite the September 11 attacks. The investment firm goes on to note that “this is almost always the view from the economics community heading into the contractions. Yet, recessions have on average been almost a full year in duration, during which real GDP shrank 2% from peak-to-trough, and the unemployment rate rose 3.5%. Fully three-quarters of the time, the recession lasted ten months or more.”

These changing economic growth forecasts are also important because they can give us a sense of the long-term prospects of the economy. For example, if the economy grew at its potential rate of 3%, output would double every 23 years instead of the 46 years it would take if growth averaged 1.5%, the average forecast for growth in 2001.

The Consequences of the Terrorist Attack on the Economy

Monetary policy is now firmly anchored to inflation targets that have proved to be attainable and sustainable, and thus credible.

David Laidler

The terrorist attacks exposed some of the assumptions that supported even the most pessimistic pre-September 11 forecasts. For example, there is no way of knowing how much the battle against terrorism will cost because of uncertainty about the intensity and duration of the conflict.

The Canada-U.S. border is a prime example of the effect of this uncertainty. While it is difficult to get a precise measure of the economic impact of slower border crossing, it is worth noting that even though the border was closed for only 20 minutes on September 11, several Canadian auto plants were forced to shut down for the afternoon, resulting in lost production for the company and lost wages for the workers. In its November Monetary Policy Report, the Bank of Canada estimated that the repercussions (on transportation, finance, tourism) of September 11 reduced third-quarter growth, measured at an annual rate, by about 1 percentage point. This means that the economy either stagnated (zero growth) or shrank by 1% in the third quarter: “While the fourth-quarter impact of the attacks on growth is more difficult to assess, it seems likely to be at least as large as the direct effects in the third quarter, suggesting that growth in GDP in the fourth quarter will be near zero.”[8] Perhaps the most worrying impact of September 11, however, is uncertainty about the duration of border delays. As several witnesses remarked, businesses may be reluctant to invest in Canada if border delays fluctuate unpredictably whenever there’s a security threat to the United States.

I think it’s wrong to think of this as being a short-run problem involving trucks being held up at the border, and that this is going to go away. Once an investor has seen that kind of shock, that investor is going to think many times about building a plant in Canada if access to the United States’ market is in doubt in the future … . What this means is that the border security issue is absolutely critical to the level of productivity in Canada and the rate of productivity growth. David Laidler, Professor, Department of Economics, University of Western Ontario

Although Canada Customs and Revenue Agency (CCRA) data suggest that cross-border traffic delays are back to normal, there is always the possibility that further terrorist attacks could lead to another round of tighter security and more permanent delays or that political sentiments in the United States could lead to stricter border security whether needed or not. Even a temporary increase in the delays — such as in the aftermath of the September 11 attack — can impose large costs. For example, the Conference Board said in a recent report that it is “not unreasonable to assume a 1% decline (at annual rates) in exports in the third quarter because of border delays, which would take roughly 0.4% out of real GDP in the quarter ….”[9]

Airline Industry

The terrorist attacks have had other very obvious impacts on particular sectors of the economy. The Canadian airline industry, which accounts for about $4 billion of real GDP and which was already in a precarious position, has seen air traffic fall off by between 20% and 30% since flights resumed on September 15. The Conference Board estimates the attack will reduce the airline industry’s real output by $500 million (at annual rates) during the third quarter. While this represents less than 1% of the economy’s total output, it is nevertheless a very serious blow to an industry that was already suffering from over-capacity.[10] Additionally, there is no question that related industries, such as tourism, have also been affected.

The economic impact of a collapse of the Airline Industry is difficult to quantify, but there is little doubt that modern economies rely heavily on deliveries of goods and people via airlines. In the aftermath of September 11, for example, a number of manufacturers were forced to shut down production because the cancellation of air traffic stranded needed parts and people.[11] Airplane manufacturers have not been immune from the slowdown or repercussions of September 11 either. In response to the fall-off in airline travel, Boeing recently announced the layoff of a third of its employees at its Arnprior, Ontario plant as part of broader move to lay off of 20,000 to 30,000 employees by the end of 2002.

The tragic events of September 11 have changed the world in which we live and work, especially for people in the airline and aerospace industries. The airline industry was already struggling as a result of the downturn in the US economy and according to our estimates, these attacks will result in significant job losses in this and in other related sectors such as major equipment and engine supplies, etc. Gilles Ouimet, President, Pratt & Whitney Canada

In the long term, I think it’s terribly important that we focus on innovative solutions to sustain aviation as a safe and secure mode of transport … . We need to maintain public confidence. Therefore, we must ensure that the aerospace research and development link is not broken by these tragic events. Peter Smith, President and Chief Executive Officer, Aerospace Industries Association of Canada

In response, the government has offered a $160 million aid package to the airline industry, and a conditional $75 million loan guarantee to Canada 3000.[12]

Nevertheless, what is bad for one sector may prove to be an opportunity for another. Short-length travel by air is being replaced by bus, car and train travel. While airlines are facing severe financial difficulties and some are facing insolvency, this does not suggest that airplanes will not fly and that airline service will not exist. Rather it means that restructuring will take place and that investors will experience the consequences of the risk that they have chosen to take by investing in airlines.

Economics Professor David Laidler made the point that the economic effects of September 11 largely represent real shocks to the economy, not a general deficit in aggregate demand. If the airline industry now possesses excess capacity because demand has shifted away from airline travel, resources should be allowed to move to other sectors. It would be a mistake, in his view, to try to prevent these adjustments from happening via demand side stimulus, or any other kind of short-term aid.

Consumer Confidence

People tend to sit and wait... What will trigger them to get moving again is very hard to say. David Dodge

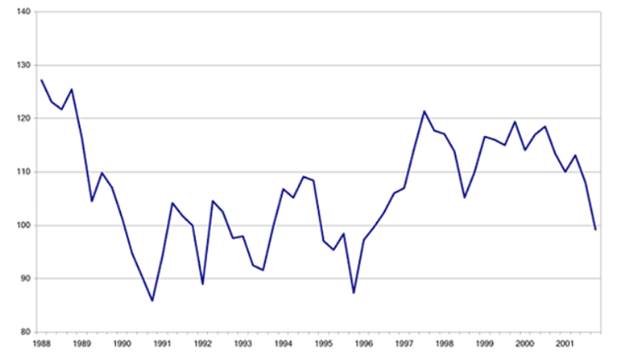

Even before the attack, there were signs that consumer confidence — which until recently had been remarkably resilient — was waning, as can be seen in Chart 3, which depicts the Conference Board of Canada’s consumer confidence index. In the U.S., the picture is even bleaker. Even before September 11, U.S. consumer confidence had fallen to an eight and a half year low. Since then, consumer confidence has risen slightly. Consumer confidence is an important indicator of the short-term outlook for the economy because it indicates the extent to which consumers are willing to spend.

Since September 11, consumer confidence has fallen even further. The Conference Board, for example, reported in its most recent survey that its Index of Consumer Confidence declined by 17 percentage points to its lowest level since 1996.[13] The questions for governments are: what is the appropriate response to this? Will consumer and business confidence be strengthened by fiscal measures that return us to a deficit in order to try to stimulate the economy or to assist ailing sectors of the economy? As Professor Laidler reminded the Committee, “Canada’s benign policy framework even now has been in place for only six years, and credibly so for a shorter period.”[14] Or will confidence be restored by measures that show a resolve to effectively deal with the terrorist threat?

Chart 3: The Conference Board’s Index of Consumer Attitudes (1991=100)

In order to assess the policy options facing the federal government, it is useful to consider three aspects to the current economic situation. The first is a decline in aggregate demand due to the prior economic slowdown and a more recent deterioration in consumer confidence. This drop is an aggregate demand shock that has been largely addressed by an unprecedented monetary stimulus and the tax cuts announced last fall in the government’s Economic Statement and Budget Update. The second is a sectoral shift in net demand. With North Americans avoiding travel in general and air travel in particular, certain sectors of the economy are facing significant, short-term excess supply problems that have led to capacity reductions, layoffs, and even the threat of insolvency for a number of firms. No amount of aggregate stimulus can alter this shift in consumer preferences, nor should the government try, since the industry should be able to solve the problem on its own. In the U.S. for example, the airline industry is taking measures to address the problem by dramatically lowering some fares. The third aspect is a reduction in productivity as security concerns transform the Canadian-American border from a nuisance to a serious barrier to Canadian prosperity.

Appropriate and effective national security initiatives can have a positive impact on all three aspects mentioned above. They can restore broad consumer and business confidence, they can restore faith in traveling, and they can restore the border to being nothing more than a nuisance. All of this will happen not because the government spends large amounts of money on security or spends so much as to go back into deficit. It will happen if government implements a security strategy that is convincing and effective.

There is a further danger, repeatedly highlighted by the U.S. Federal Reserve, that the terrorist attack’s economic effects would manifest themselves through the wealth effect: “Negative wealth effects from falling stock market prices, declining payrolls, and sluggish income gains — should they persist — might well depress consumer expenditures over coming months.”[15] In Canada, most studies suggest the wealth effect is less pronounced than in the United States.[16] The Royal Bank calculates the Canadian wealth effect at about 2 cents per dollar of wealth gained or lost compared with 4.4 cents in the United States. The IMF estimated that a 35% drop in equity prices could reduce consumption by $5 to $10 billion, or 0.5% to 1% of GDP in the long term.[17]

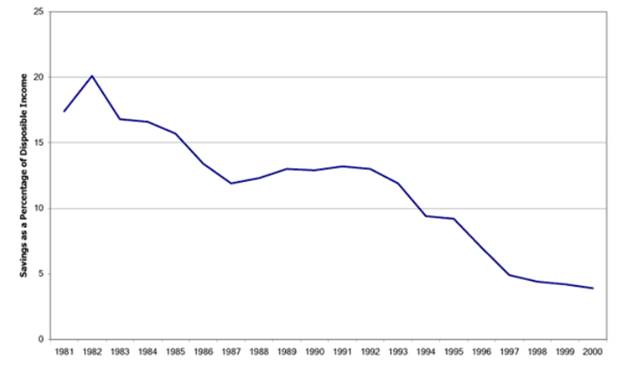

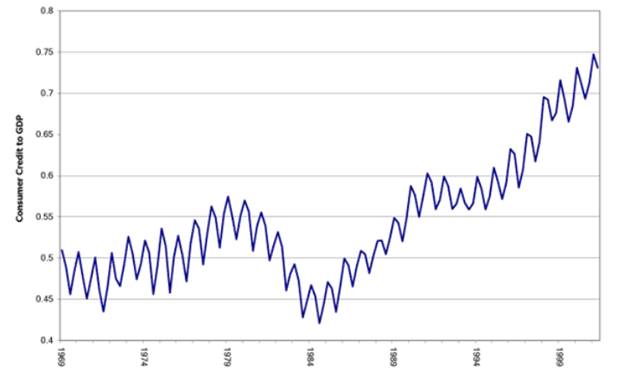

A final danger from the consumer’s vantage point is the high levels of consumer debt and the low household savings rate. Consumer credit is at 70% of GDP and savings rates are at the lowest level since Statistics Canada started tracking this variable in 1961. This is offset by the fact that, despite high debt levels, debt servicing costs are now at historical lows due to low interest rates. Nevertheless, some consumers are being cautious because of their vulnerable employment status.

On the other hand, total savings of the economy, the primary source of investment capital, are in better shape, reflecting the sharp turnaround of government finances in the last third of the 1990s. However, with the possibility of reduced surpluses and further short-term consumer indebtedness because of the economic slowdown, total savings could begin to fall.

What we’re looking at now is a kind of demand weakness arising from perhaps over-investment and consumers getting overstretched in the United States. Thomas Wilson, Director, Policy and Economic Analysis Program, University of Toronto

A Synchronized Global Economic Cycle

Perhaps one of the biggest dangers of this slowdown is the fact that, unlike the Mexican peso crisis or the Asian financial crisis, the current economic slowdown is affecting all the major economies of the world at the same time and this synchronized cycle was only made worse by the terrorist attack of September 11. As Kenneth Rogoff, the International Monetary Fund’s Economic Counsellor and Director of the Research Department said in a recent press conference, “this synchronized slowdown has reflected stronger than expected global linkages.”[18] There is a danger then that the slower growth that began in the United States and spread to Canada, Europe and Southeast Asia could be exasperated as slower growth elsewhere works its way back to the United States. Even before September 11, the IMF had reduced its projection for 2001 growth by more than 0.5 percentage points to 2.6%, with a similar reduction for the 2002 projections to about 3.5%. The IMF does not expect the events of September 11 to alter fundamentally its 2001 projections although it does expect 2002 growth to come in somewhat less than expected.

Chart 4: Saving Rate

Chart 5: Ratio of Consumer Credit to GDP

Monetary Policy and the Financial Sector

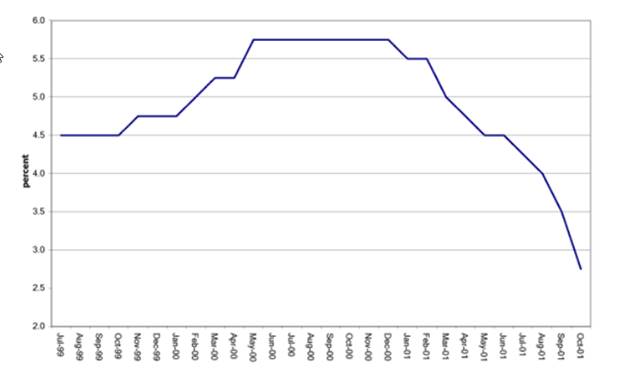

Counterbalancing these economic negatives, however, are the stimulative effects of monetary and fiscal policy. Since the attack, the U.S. Federal Reserve has cut its overnight interest rate by 150 basis points. The Bank of Canada meanwhile has reduced its overnight benchmark rate by 125 basis points since September 11. This aggressive stance suggests the Bank has grown increasingly concerned about the near-term outlook for the economy. Chart 6 shows that the overnight interest rate, which sets the tone for other interest rates such as mortgage and general loan rates, has been reduced by 300 basis points since the beginning of the year. It is generally assumed that the stimulus effect on investment and consumption from lower interest rates can take as long as 18 to 24 months to make itself fully felt.

While monetary policy is playing an important role in stimulating the economy, there is a danger that the slowdown could lead to credit-rationing by the commercial banks, as fewer and fewer firms meet normal loan criteria. In its November Monetary Policy Report, the Bank of Canada said this is already happening at least in part because of heightened uncertainty about the economic outlook. “In the bond market, this tightening has been reflected in the increase in spreads between the interest rates on corporate debt and those on government debt. Moreover, whereas earlier in the year, only a few sectors, such as telecommunications and automotive manufacturing, had been affected, more industries are now feeling the effects of the tighter credit conditions.” The Bank goes on to note that there has been a corresponding increase in the demand for credit as firms seek to hold greater cash balances in the face of heightened uncertainty about the future.

Fiscal Policy

On the fiscal side, the U.S. government has announced a series of spending initiatives — coupled with tax measures passed earlier this year — that in total are expected to amount to about 1% of U.S. GDP. This stimulus will benefit Canada to the extent that it succeeds in restoring U.S. consumer confidence and leads to an increased demand for Canadian exports. The first tranche of this stimulus package came in the form of income tax rebates worth $38 billion mailed out in July. The rebate was part of a larger tax cut, spanning ten years and totalling over US $1.2 trillion.

The Committee wishes to point out that Canada has already provided a strong degree of fiscal stimulus in 2000, equivalent to more than 2% of GDP.

Chart 6: The Evolution of the Bank of Canada’s Overnight Interest Rate Target

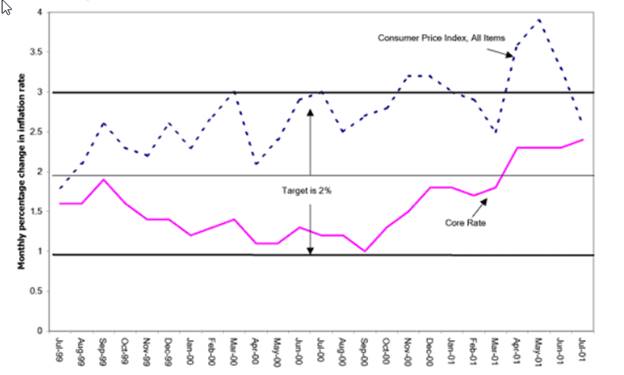

Chart 7: The Evolution of Inflation Rates (Total CPI and Core CPI) Relative to the Bank’s 2% Target

In the United States, immediately after the attack, legislation was passed giving the government the authority to spend a further $40 billion to assist areas directly affected by the attack, fight terrorism and increase various forms of security including that of the transportation sector. Later in September, the U.S. announced a $5 billion package to assist its airlines and another $10 billion in loan guarantees. Early in October, U.S. Treasury Secretary Paul O’Neill told the U.S. Finance Committee that his department was drafting plans to spend another $60 to $75 billion in 2002, again to stimulate the economy and restore consumer confidence.

While it is difficult to say how much of an overall stimulus effect these expenditures will have, they will undoubtedly have some beneficial impact for those sectors directly targeted, namely the airlines industries, building materials sector and the security sector (e.g., firms that provide security services such as security guards, alarms and other security devices). It is important to stress, however, that the money to finance these spending increases must come from somewhere. In other words, the $40 billion injection into the building trades and security sector means there is $40 billion less for debt reduction, tax cuts or other spending increases. The net effect of the additional spending and tax cuts depends very much then on how the money could have been otherwise used.

Similarly, additional military spending by the U.S. to finance its war on terrorism could provide a shot in the arm to the arms manufacturers in the U.S. and related industries, although again this kind of spending necessarily means foregoing some other combination of debt reduction, tax cuts or spending increases that reflected different spending priorities and may have been more productive. It is also important to note that military spending is qualitatively different from most other types of expenditure since the goods generated (tanks, aircraft, etc.) generally cannot be used for any other purpose, permanently consuming scarce resources and adding little to society’s productive capacity.

Given the unprecedented magnitude of the recent monetary stimulus in Canada and the United States, there is a growing debate on both sides of the border about whether there is a need for an additional fiscal stimulus.[19] Government spending on security is not designed to provide fiscal stimulus. It is there to provide social capital. Professor Laidler told the Committee in his written submission that monetary stimulus is just starting to have an effect and the need for further stimulus on the fiscal side is not evident. Moreover, would new fiscal measures actually stimulate the economy, especially if they lead to a recurrence of deficits and tarnish the government’s reputation for sound economic management?

According to Professor Laidler, “The single most important factor lending credibility to Canadian monetary policy in recent years has been the remarkable turnaround in the fiscal situation which the 1995 and subsequent budgets brought about. It is an elementary proposition that low inflation cannot be permanently sustained in the face of a perpetually rising debt to GDP ratio…when deficits disappear, low inflation becomes more credible, and that leads to lower interest rates and a better real economic performance. In turn, these effects make the budget easier to handle, and a virtuous policy circle is set in motion.” The downside risk of measures that might not be effective is then very high. Moreover, it should not be forgotten that the federal tax cuts of 2000 have already provided a fiscal stimulus equal to about 2% of GDP.

Long-term Prospects: The Benefits of and Need for Sound Fundamentals

While it is important not to underestimate the impact of the economic slowdown and the consequences of September 11, it is also crucial to keep a long-term perspective. As the 1997-98 Asian financial crisis showed, strong fundamentals — balanced budgets, low inflation and correspondingly low interest rates, internationally competitive firms on the cutting edge of modern technology — bode well for a robust recovery.

The federal government has demonstrated strong leadership in the area of debt reduction, retiring more then $33 billion of federal debt in the past four years, — $27 billion of this the last two years alone.

Insurance Bureau of Canada

Consumer Prices

In the first few months of 2001, the Consumer Price Index (CPI) — a gauge of the cost of a normal basket of consumer goods — grew almost 4%, well above the Bank of Canada’s upper limit of 3%, as can be seen in Chart 7. The surge was driven mostly by higher energy prices. By early summer, however, energy prices had started to fall, pulling the CPI back below 3%. (In the shorter term, the Bank looks to trends in “core inflation,” — CPI minus energy and food prices, and indirect taxes — which is not as volatile as total inflation. In the long term, however, it is total inflation that affects Canadians purchasing power and is the relevant variable for monetary control. The Bank is also now giving more prominence to the midpoint target of 2%, implicitly suggesting that 3% inflation is unacceptably high.)

Debt

IBAC commends the federal government for its conviction and performance in soundly managing the economy in recent years. There’s a lot of great news in its four consecutive budget surpluses, its commitment to a five-year tax reduction plan, and the tangible progress made in the reduction of the national debt.

Ginny Bannerman, Insurance Brokers Association of Canada

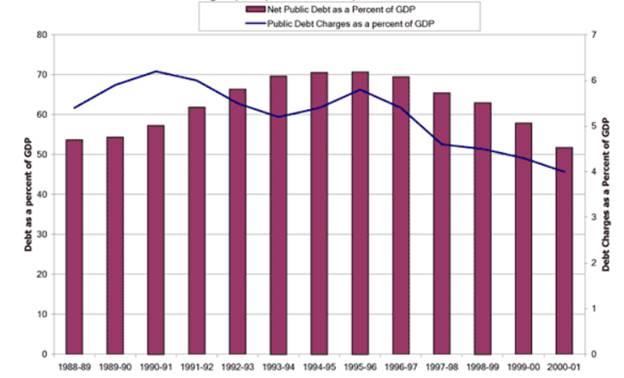

Notwithstanding the slowdown in economic growth, the government continued to make important gains in reducing the country’s debt burden as measured by the ratio of the federal government’s net public debt (total debt minus the government’s financial assets) to GDP, shown in Chart 8. The ratio stood at 51.8% at the end of fiscal 2000-01, down from a high of 70.7% in 1995-96. Similarly, debt servicing costs as a percent of GDP have fallen to 4% of GDP, their lowest level since 1980-81 in part because of lower overall debt levels, lower interest rates and stronger economic growth. In absolute terms, this translates into an ongoing saving of $2.5 billion each year in interest payments, money which can be used to finance tax cuts and pay for new initiatives and help the economy weather the current economic storm. In fiscal 2000-01, debt-servicing charges ate up $43.1 billion, or 23.5% of the government’s total revenue, down from $41.65 billion, or 25% of total revenue, in 1999-2000.

We certainly have seen, since last summer, a decline in the economic expectations of the small business sector. Nevertheless, we’ve seen, since the events of September 11, quite a stabilization in the outlook of small firms across the country and indeed the sector remains more optimistic than pessimistic. … We see overall our members having a pretty “steady as you go” reaction to the current economic environment.

Catherine Swift, Canadian Federation of Independent Business

Chart 8: Net Public Debt and Charges (as a percent of GDP)

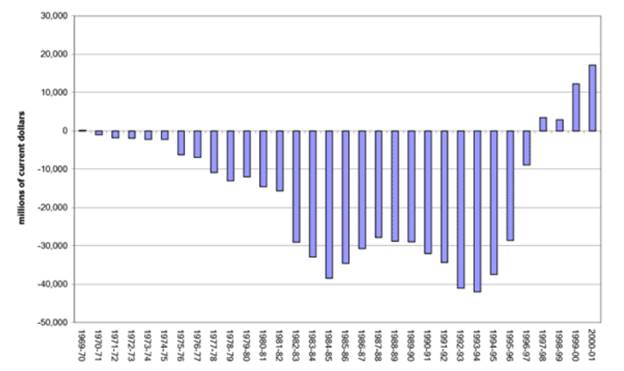

Chart 9: Canada’s Budget Balance Since the 1969-1970 Surplus

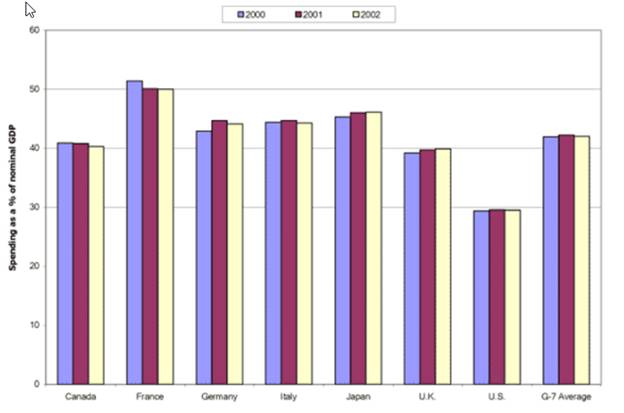

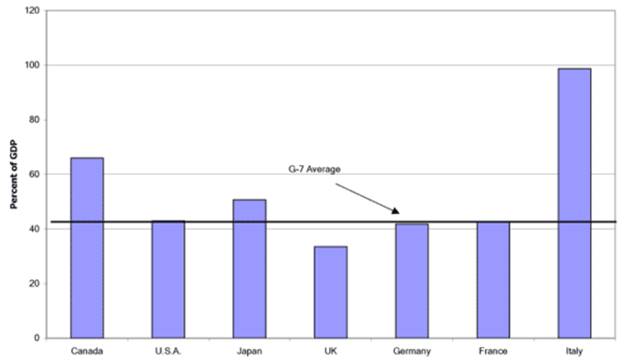

Chart 10: Government Spending as a Percentage of GDP in G-7 Nations

Budget Balance

In 1997-98, the federal government recorded a surplus of $3.5 billion, its first since 1969-70. This was followed by surpluses of $2.9 billion in 1998-99, $12.3 billion in 1999-2000 and $17.1 billion in 2000-01.[20] Chart 9 shows how the government’s budget balance has evolved during the last 30 years.

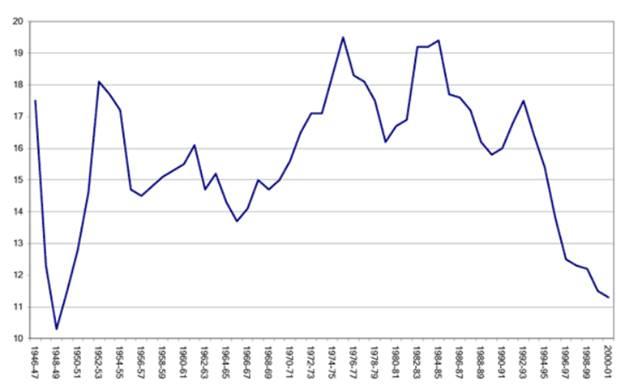

Charts 10 and 11 show how Canada has fared compared to other G-7 nations. Much of the turnaround from chronic deficits to healthy surpluses occurred because of deep spending cuts in the mid-1990s. For example, total spending (including debt servicing costs) in 2000-01 of $119.4 billion was 2.6% lower than the $122.6 billion spent seven-years earlier in 1992-93. Most of the cutbacks, however, occurred in program spending. The ratio of program spending to GDP fell to 11.3% in 2000-01, its lowest point since just after World War II.

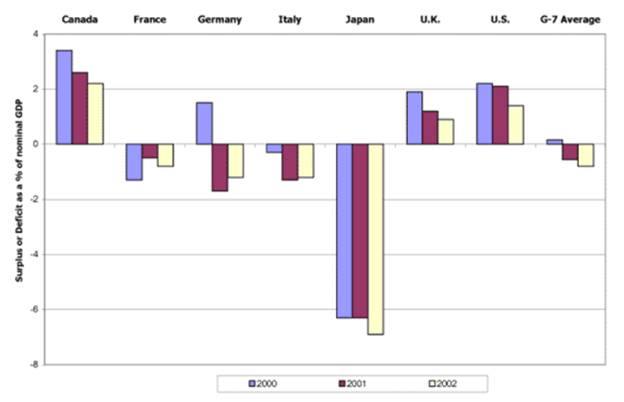

Chart 11: Government Financial Balances – Data for 2001 and 2002 are Projections Made Before September 11.

Chart 12: Federal Program Spending as a percent of GDP

Chart 13: Total Government Net Debt in 2000 (National Accounts Basis)

Source: OECD Economic Outlook No. 69 (June 2001). Department of Finance Calculations. Canadian data are overstated relative to countries that have large unfunded liabilities for government pensions. Among the G-7 countries, only the United State’s data are comparable with those of Canada.

Indeed, much of the longer-term optimism expressed by most forecasters rests on the belief that these fundamentals are still largely in place. Stimulus from lower interest rates and tax cuts, sustained consumer spending, and a stronger U.S. economy are expected to have their desired effect by the middle of the next year. Forecasters also point out that many of the factors that contributed to past recessions are noticeably absent: expectations of high inflation reflected in rapid real estate price increases have not been evident,[21] the government’s fiscal position is relatively healthy, and a relatively benign inflation rate allows the Bank of Canada some scope to lower interest rates as needed. Similarly strong fundamentals seem to be at work at the global level. For example, the Conference Board of Canada in its Fall Economic Update noted that “a key indication of the depth of an impending slowdown is the extent of excessive or unsustainable activity preceding the slowdown. Few such excesses preceded the growth slowdown, suggesting that the weakness will be short-lived.” The IMF’s Kenneth Rogoff recently noted also that “While there are clearly substantial uncertainties about unfolding events, one should not overlook that the economic fundamentals in many countries and in many respects have improved in recent years, and from an economic perspective, this leaves the world somewhat less vulnerable than it otherwise might be.” In summary, the risks to the economy are not due to failures of government policy but rather to developments in the real side.

[1] This figure reflects all measures up to and including the 2000 Economic Statement and Budget Update.

[2] “Remarks by David Dodge, Governor of the Bank of Canada, on Current Developments in the Canadian Economy.” Bank of Canada, 21 September 2001. http://www.bankofcanada.ca/en/speeches/sp01-7.htm

[3] House of Commons, Standing Committee on Finance, First Report, Budget 2000: New Era…New Plan, 2nd session, 36th Parliament, December 2001.

[4] The Bank of Canada has estimated that given population and productivity growth the Canadian economy can “safely” grow between 2.75% and 3.25%, with 3% representing the midpoint of this estimate.

[5] The figure would be closer to 1.84% if not for an “outlier” prediction by the Bank of Nova Scotia, which expects economic growth of 0.6% in 2002.

[6] TD Economics, Report on Canadian Government Finances, “Federal and Provincial Fiscal Outlook to 2005-06,” October 12, 2001. The TD Economics projections represent the status quo and are based solely on economic factors. It includes government tax and spending initiatives mentioned in past budgets and economic statements. No discretionary changes are assumed, although the impact of lower growth on revenues and non-discretionary spending is taken into account. It does not include recently announced security measures.

[7] Patrick Grady, The Case for a Fiscal Deficit After September 11, Submission to the Standing Committee on Finance, November 2001. The government planned to set aside $3 billion for its contingency reserve, which is used to pay down the debt if not needed, and $1 billion for economic prudence in case of unforeseen economic disruptions. The planning surplus represents funds over and above these amounts.

[8] Bank of Canada, Monetary Policy Update, November 2001, p. 12. http://www.bankofcanada.ca/en/pdf/mprnov01.pdf.

[9] Implications of the Terrorist Attack for the Canadian Economy: Special Report,” Conference Board, September 19, 2001.

[10] Ibid.

[11] According to the Canadian Economic Observer, October 2001, p. 1.10, “nearly 40% of U.S. exports are sent by air cargo, notably high-tech goods.”

[12] Canada 3000 was unable to make use of the loan guarantee. It has recently filed for bankruptcy.

[13] These data are not reflected in Figure 3, which contains survey data from the week of September 11 and the week before. The Conference Board decided to update its survey because it felt these data did not accurately reflect the full impact of September 11.

[14] David Laidler, “Notes for the Standing Committee on Finance,” August 1, 2001, p. 3.

[15] United States, Federal Reserve Board, “Minutes of the Federal Open Market Committee,” 21 August 2001. http://www.federalreserve.gov/fomc/minutes/20010821.htm.

[16] The Federal Reserve said its decision to reduce interest rates by 50 basis points on April 18 was based in part on this concern. This was a startling statement since consumption, which represents roughly 58% of all economic activity in Canada, usually holds up well during all but the most prolonged downturns. Only the recessions in 1981 and 1990 saw significant weakness in consumption. “In fact, in numerous instances, consumer spending accelerates after a mild downturn begins.” See Philip Cross, “Expenditure on GDP and Business Cycles,” Canadian Economic Observer, March 2001, p. 3.15.

[17] This calculation appears to be in line with work done by the Bank of Canada.

[18] Kenneth Rogoff, Press Conference, International Monetary Fund, Washington, D.C., 26 September 2001, http://www.imf.org/external/np/tr/2001/tr010926.htm.

[19] Milton Friedman, “No more stimulus needed — Big fiscal moves would be a big policy mistake,” National Post, 11 October 2001, p. FP19.

[20] These budget data are presented on a modified accrual basis. On a “full accrual basis,” or financial requirements basis, the government has run a surplus since 1996-97. Beginning next year, all government budget data will be presented on a full-accrual basis.

[21] Surging real estate prices can be an indicator of inflationary expectations and could therefore lead to tighter monetary policy (i.e., higher interest rates).